Summary

- Vodafone’s £4.3bn buyout of CK Hutchison’s stake cements a three-operator UK market and gives VodafoneThree unified control to accelerate integration, investment and execution.

- Scale offers the potential for faster decisions, cost synergies and a stronger 5G SA rollout, but consolidation must translate into better coverage, reliability, value and digital experiences to be judged a success.

- A major part of that test will be how effectively VodafoneThree modernises operations, automates service layers, incorporates AI and reduces legacy stack complexity.

- MVNOs will face tighter, more strategic wholesale dynamics and must differentiate beyond price through sharper propositions and superior digital journeys, while VodafoneThree’s multi-brand approach must deliver genuine choice.

- Regulators and the market will measure outcomes against clear commitments, making execution, not just ownership, the decisive factor.

Introduction

On 5 May 2026, Vodafone announced an agreement to buy out CK Hutchison Group Telecom Holding Limited’s stake in the VodafoneThree joint venture for £4.3 billion (€4.9 billion), through a cancellation of shares. Once complete, Vodafone will become the sole owner of VodafoneThree, subject to approvals under the UK National Security and Investment Act, with completion expected in the second half of 2026. This Vodafone CK Hutchison agreement underscores the push toward ‘VodafoneThree full ownership.’

This follows the merger of Vodafone UK and Three UK, which was completed on 31 May 2025, forming VodafoneThree UK. Vodafone currently owns 51% of VodafoneThree, with CK Hutchison holding the remaining 49%.

But while the ownership structure is changing, the regulatory implications are significant. Full ownership raises questions about how competition will be maintained and monitored, especially given the UK’s focus on preventing market dominance. Addressing these concerns helps the audience understand the broader regulatory landscape and potential market impacts.

Not Just Ownership, But Control

In telecoms, ownership matters because control matters.

A joint venture can deliver scale, but it also comes with complexity. Shared governance, competing shareholder priorities and slower decision-making can make execution harder, especially when the business is trying to integrate networks, rationalise operations, improve service quality and deliver a major infrastructure programme at the same time.

Full ownership gives Vodafone a simpler route. One shareholder. One strategy. One chain of accountability.

Vodafone has positioned the deal as a way to accelerate progress and accelerate the transformation of the UK’s digital infrastructure. The company projects saving £700 million annually in costs and capital expenditure by FY30. The transaction values VodafoneThree at an enterprise value of £13.85 billion.

That tells us something important about the next stage of UK telecoms. The winners won’t simply be the operators with the most spectrum, customers or retail brands. They’ll be the operators responsible for reliability service quality.

The Promise of Scale Is Still Just a Promise

The argument for consolidation has always been straightforward: fewer, stronger operators should be able to invest more, build better networks and compete on quality rather than being trapped in a cycle of thin margins and underinvestment.

That was central to the original Vodafone and Three merger case. The merged business committed to an £11 billion network investment plan, with VodafoneThree saying it will build the UK’s best network and reach 99% 5G Standalone population coverage by 2030 and 99.96% by 2034.

Telecoms is capital-intensive. 5G Standalone, network densification, automation, fibre backhaul, AI-driven operations and digital service layers all require significant investment. Scale can help fund that investment, but the harder task is turning it into simpler architecture, cleaner data flows and faster service delivery.

However, while consolidation aims to deliver better networks and investment capacity, there is a risk that these benefits may not materialise without effective execution and regulatory oversight. That risk becomes sharper when modernisation depends on complex integration work, from legacy stack simplification to AI-enabled operational change.

The CMA‘s original investigation into the Vodafone and Three merger found that combining two of the UK’s four mobile network operators could lead to higher prices, reduced services, and weaker wholesale terms for MVNOs. The deal was ultimately cleared with legally binding commitments, ensuring safeguards that protect consumer interests and market fairness.

The industry shouldn’t assume that consolidation automatically equals progress. It only becomes progress if the benefits, such as better coverage, reliability, value and digital experiences, are clearly realised and delivered.

This is where the distinction between scale and impact becomes crucial. Hamish White, CEO of Mobilise, puts it this way:

The real test of telecom consolidation is not how much scale an operator gains, but how effectively it converts that scale into better customer experiences, faster innovation and stronger wholesale partnerships. In a three-network market, MVNOs will need to compete on agility, digital experience and proposition clarity rather than price alone.

Hamish White, CEO of Mobilise

This captures the core challenge for VodafoneThree. Full ownership may simplify decision-making, but the market will judge the business on whether it uses that control to improve the experience for customers, partners and wholesale clients.

The Pressure on MVNOs Will Increase

One of the most important consequences of this deal may be felt outside VodafoneThree itself.

The UK mobile market has a strong MVNO ecosystem, with brands competing on price, flexibility, niche propositions and customer experience. MVNOs rely on wholesale access to mobile networks, which means the balance of power between network owners and virtual operators matters.

The CMA has already acknowledged this risk. Its guidance noted that reducing the number of available network operators from four to three could make it harder for wholesale customers to secure competitive terms and offer the best deals to retail customers.

That doesn’t mean MVNOs are suddenly in trouble. But it does mean the wholesale environment is likely to become more strategic, more competitive and potentially more constrained over time.

For MVNOs, differentiation can no longer rely on pricing alone.

If wholesale economics become tighter, MVNOs will need to compete through sharper propositions, stronger brand positioning, better onboarding, more flexible digital experiences and value-added services. They will need to understand their customer segments deeply and build products around them, whether that means travel connectivity, family plans, business communications, international calling, eSIM-first experiences, or bundled digital services.

In a market with fewer infrastructure owners, agility is an advantage.

RECOMMENDED READING

MVNOs and MVNEs – A Strategic Guide to Telecom Innovation and Growth

Multi-Brand Strategy: Continuity For Now, Questions for Later

Vodafone has said there will be no change to VodafoneThree’s multi-brand strategy, maintaining continuity across Vodafone UK, Three UK, VOXI Mobile, SMARTY and Talkmobile.

That makes sense in the short term. These brands serve different parts of the market. Vodafone has enterprise strength, a premium consumer position and strong convergence ambitions. Three has historically been a challenger brand associated with data-heavy plans. VOXI and SMARTY play into digital-first and value-conscious segments.

However, maintaining multiple brands isn’t the same as maintaining multiple competitive forces.

The real question isn’t whether the logos survives. It’s whether those brands continue to create meaningful choices for customers.

If VodafoneThree can use its portfolio to serve diverse customer needs clearly, it could strengthen the market. If the brands become a surface-level segmentation layered over increasingly similar pricing and product structures, customer choice may feel narrower over time.

This is where execution will matter.

A multi-brand strategy only works when each brand has a clear role, a distinct customer promise and the operational flexibility to serve its audience properly.

The Customer Experience Test

The telecoms industry often talks about infrastructure first. That’s understandable. Networks are the foundation. Without coverage, capacity and reliability, everything else collapses.

But customers don’t experience a merger through network architecture diagrams. They experience it through signal strength, billing accuracy, app usability, support quality, onboarding, roaming, plan flexibility and how quickly issues get resolved.

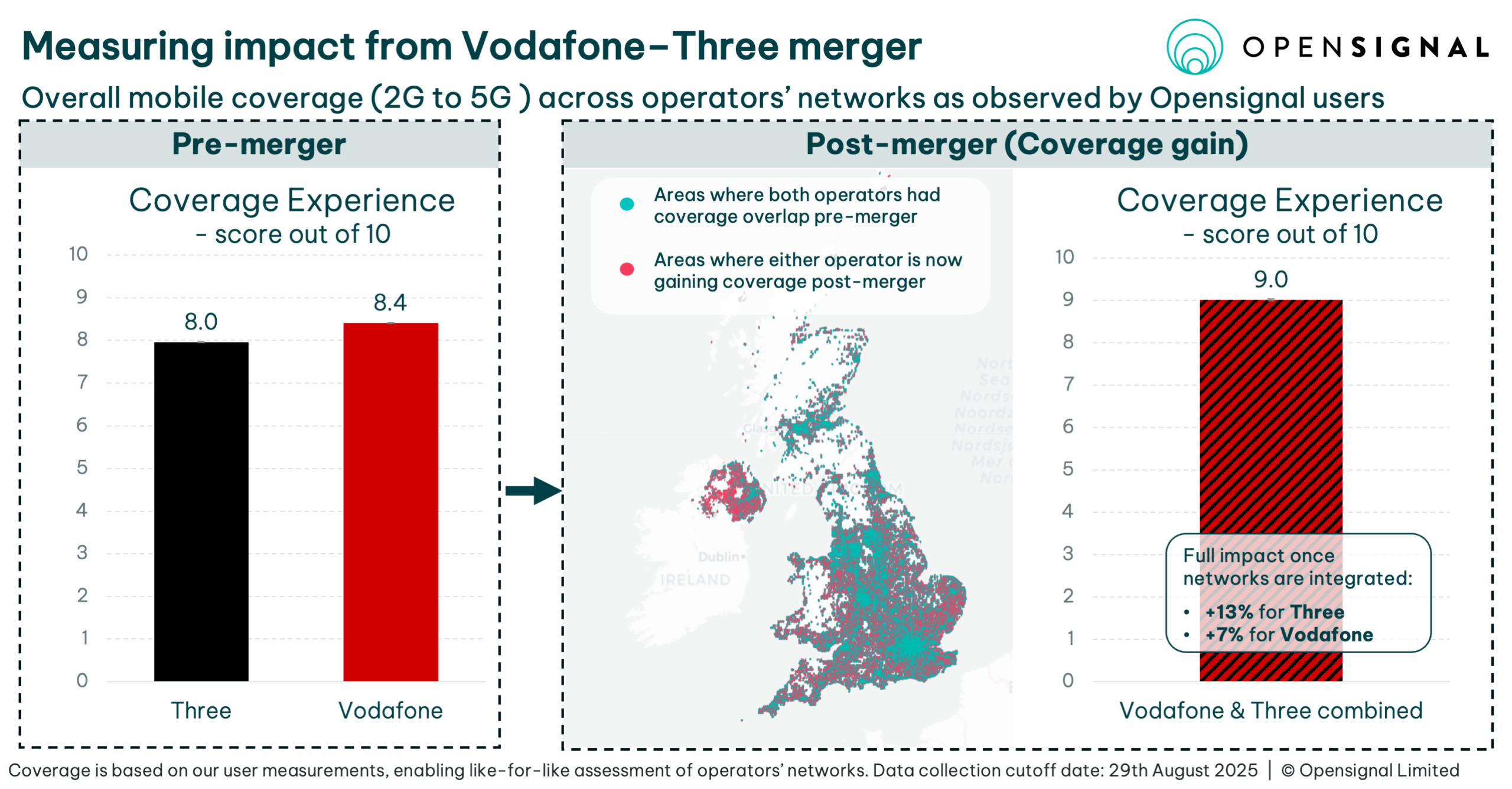

An analysis by OpenSignal shows that the Vodafone-Three merger significantly enhanced overall Coverage Experience (across 2G to 5G) due to network integration. Three users experienced a 13% boost in coverage, while Vodafone users experienced a 7% increase compared to before the merger.

Source: OpenSignal

Source: OpenSignal

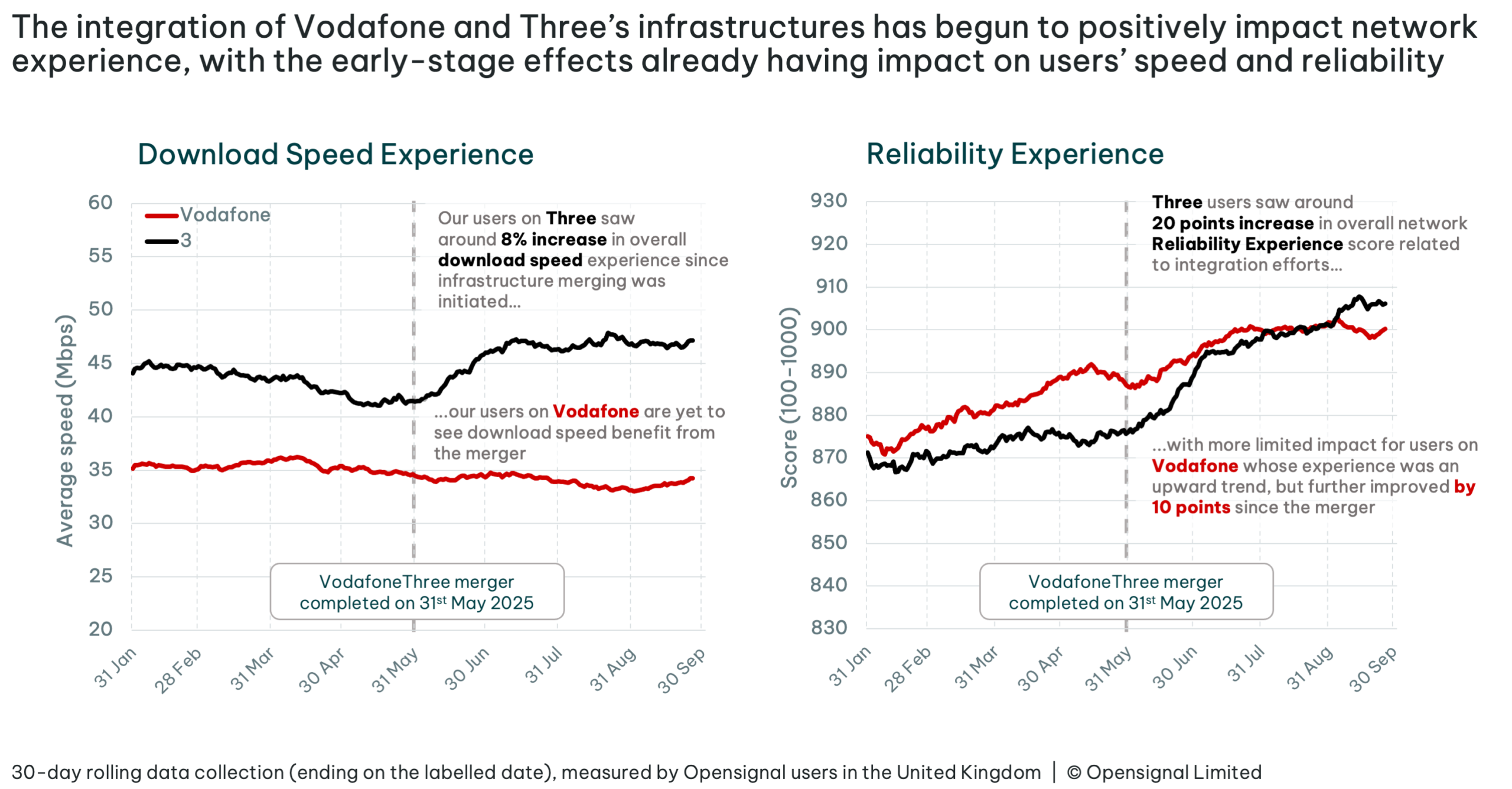

Regarding reliability, improvements became evident on Three’s network, with Download Speed Experience increasing by 8%, from 43.16 Mbps in Q2 2025 to approximately 46.72 Mbps in Q3. Both Vodafone and Three users now enjoy more reliable networks after the merger. Three users’ Reliability Experience score improved by 20 points, from 876 in Q2 2025 to 897 in Q3 2025. Vodafone users’ scores rose by 10 points, from 887 in Q2 2025 to 897 in Q3 2025.

Source: OpenSignal

Source: OpenSignal

That’s why VodafoneThree’s next challenge is operational, digital and experiential. A major part of success will depend on how effectively it modernises operations, automates service layers, incorporates AI and reduces legacy stack complexity.

- Can customers move between products without friction?

- Can digital journeys become simpler?

- Can AI support faster, more personalised service without making the customer journey feel impersonal?

- Can network, billing and care systems work from cleaner, more unified data?

- Can support teams access accurate, unified customer data?

- Can the operator reduce legacy complexity while keeping services stable?

- Can business customers and MVNO partners get faster, clearer and more reliable service?

These questions will determine whether this deal is remembered as a smart consolidation or simply as market concentration. If VodafoneThree can use AI to remove friction, predict issues and automate routine service journeys, it can make scale visible to customers. If AI is layered on top of fragmented legacy systems without simplification, the impact will be limited.

The Wider Lesson For Telecoms

Vodafone’s buyout of CK Hutchison’s stake is part of a bigger industry pattern. Telecoms operators are under pressure to invest heavily while managing high costs, demanding customers, regulatory scrutiny and intense competition from digital-native service providers.

In that environment, consolidation becomes attractive. But consolidation isn’t a strategy in itself. It’s a platform for strategy.

The operators that succeed will be those that use scale to simplify, modernise and innovate. That means investing in networks, but also in AI-enabled operations, automated service layers, shared data foundations, and the digital capabilities that surround them.

For the wider telecoms market, this deal reinforces three lessons.

- First, the infrastructure advantage is becoming harder to separate from the operational advantage. Owning a large network is valuable, but only if the organisation can run it efficiently, automate intelligently and translate it into better services.

- Second, MVNOs and digital telecom brands need to sharpen their differentiation. As wholesale dynamics evolve, customer experience, speed to market, AI-enabled service quality and proposition design will become even more important.

- Third, regulators will continue to watch the gap between promised investment and delivered customer benefit. The CMA’s approval of the original merger came with clear commitments, and those commitments will remain central to how the market judges VodafoneThree’s impact.

The Point Of No Return

Vodafone’s move to full ownership marks a point of no return for the UK mobile market.

The question now is whether a three-player market can deliver better outcomes.

VodafoneThree has the scale, investment plan and strategic control to make a strong case. But the burden of proof now sits with Vodafone. It must show that consolidation can produce more than cost savings and shareholder value. It must show that it can modernise operations, simplify legacy systems, use AI responsibly and improve the everyday connectivity experience for consumers, businesses and wholesale partners.

If it succeeds, the VodafoneThree deal could become a blueprint for how telecom consolidation supports national digital infrastructure.

If it fails, it’ll strengthen the argument that fewer operators simply means fewer choices.

The market has consolidated, and now it has to deliver.

Frequently Asked Questions

Question: What does Vodafone’s full ownership of VodafoneThree actually change?

Short answer: It replaces joint-venture complexity with single-owner control, enabling faster decisions and clearer accountability. As a JV, VodafoneThree had shared governance and potentially competing priorities, which can slow integration and transformation. Full ownership gives Vodafone one shareholder, one strategy and one chain of accountability. The company is framing this as a way to accelerate integration, capture £700m in annual cost and capex by FY30 and execute more decisively. Strategically, it also cements the UK’s shift from four to three mobile network operators, making scale, efficiency and execution the primary battlegrounds.

Question: How does this deal affect the UK’s 5G rollout and wider network investment?

Short answer: It strengthens the case for scale-backed investment, but it doesn’t guarantee outcomes. Execution will be judged on coverage, reliability, customer experience and operational modernisation. The merged business has committed to an £11bn network plan, including delivering 99% 5G Standalone population coverage by 2030 and 99.96% by 2034. Scale can help fund 5G SA, densification, automation, fibre backhaul and digital service layers. However, the promise of scale must translate into visible improvements, including better coverage and performance, simpler digital journeys and more reliable service. Otherwise, consolidation will be seen as concentration rather than progress.

Question: What are the regulatory and competition implications, and will prices rise?

Short answer: Regulators flagged risks but cleared the merger with binding safeguards; outcomes will be monitored against commitments. The CMA warned that moving from four to three operators could raise prices, reduce services and weaken MVNO wholesale terms. Clearance came with legally binding conditions: deliver the joint network plan, apply tariff caps for selected mobile plans and offer pre-set wholesale prices and contract terms for three years. The market will judge VodafoneThree on whether promised investment converts into better coverage, value and digital experiences. Ownership alone won’t satisfy regulators or consumers.

Question: What does this mean for MVNOs?

Short answer: Expect a more strategic and potentially tighter wholesale environment; MVNOs must differentiate beyond price. With fewer host networks, negotiating leverage may shift, and wholesale terms could become more selective. MVNOs that win will pair sharp propositions and brand positioning with superior digital onboarding, flexible plan design and value-added services. Focus areas include eSIM-first experiences, travel connectivity, family plans, business communications, international calling and bundled digital services. In a three-operator market, agility and customer experience become the MVNO’s core advantages.

Question: Will VodafoneThree keep multiple brands, and will customers still have real choice?

Short answer: The multi-brand strategy continues for now, covering Vodafone UK, Three UK, VOXI, SMARTY and Talkmobile. But genuine choice depends on distinctive roles and execution. Keeping logos isn’t enough. Each brand must have a clear promise, serve a defined segment and retain operational flexibility. Success will be measured by what customers feel: smoother movement between products, simpler apps and journeys, accurate and unified support, reduced legacy complexity and better service for businesses and MVNO partners. If brands converge on similar pricing and products, perceived choice could narrow over time.

Question: Why does AI matter in this story?

Short answer: AI could be one of the ways VodafoneThree turns scale into better service, but only if it sits on modernised operations and cleaner data. The opportunity is not simply to add chatbots or automate isolated processes. It is to use AI across network operations, customer care, billing, onboarding and wholesale support to predict issues, remove friction and speed up decision-making. If AI is layered on top of fragmented legacy systems, it could add complexity rather than remove it.

Question: What’s the timeline and financial outline of the buyout?

Short answer: Announced on 5 May 2026, the £4.3bn buyout (via share cancellation) is expected to complete in H2 2026, subject to UK National Security and Investment Act approvals. Vodafone will become the sole owner of VodafoneThree. The company targets £700m annual cost and capex by FY30, and the transaction implies an enterprise value of £13.85bn for VodafoneThree.