Everyone is talking about the SpaceX IPO. The headlines focus on valuation, while the noise focuses on Elon.

But if you strip it back, this is one of the most important infrastructure stories unfolding right now. Not just in space, but also in telecoms, AI, and global connectivity.

Here is the breakdown that matters.

1) Starlink is The Engine

Start with the simplest truth. Starlink is now the business.

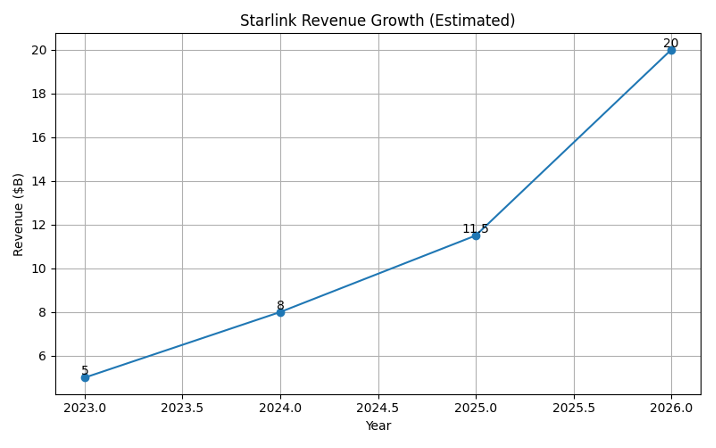

Estimates suggest Starlink generated around $7.5B to $8B of revenue in 2024, growing to roughly $11B to $12B in 2025. That is over 50% growth at scale.

This is not early-stage growth anymore. This is a business already operating at multi-billion dollar revenue with strong momentum.

The forward curve is where it gets more interesting.

Some forecasts point to around $15B of revenue by 2026. If that plays out, Starlink will effectively double its revenue in a two-year period. At that point, you are no longer looking at a satellite product. You are looking at one of the largest global connectivity platforms.

For telecoms, that is the real shift. Starlink is moving from edge case to core infrastructure.

Figure 1 – Starlink is scaling like a top-tier tech platform, not a traditional telecom asset

Figure 1 – Starlink is scaling like a top-tier tech platform, not a traditional telecom asset

2) The Moat is Launch, Not Satellites

A lot of the conversation focuses on the constellation. Thousands of satellites, global coverage, low latency. But that is not the real advantage. The real moat is rockets.

SpaceX controls:

- Launch frequency

- Launch cost

- Launch capacity

And crucially, it uses that capacity for itself. That means it can deploy and refresh its network faster and cheaper than anyone else. This is not something a telco can replicate.

It is not something most satellite players can replicate either. Amazon Kuiper is the closest challenger, and it is credible. But it is still earlier in its deployment cycle and does not yet have the same integrated launch cadence.

This is what makes the Starlink model so powerful.

It is not just a network. It is a network built on top of proprietary infrastructure that compounds its advantage over time.

3) This is No Longer Just a Telecom Story

The xAI acquisition changes the narrative in a big way.

Before, SpaceX could be understood as:

- A launch provider

- A satellite connectivity provider

- A government contractor

Now, it is becoming something broader.

A vertically integrated platform that combines:

- Connectivity through Starlink

- Government and defence services through Starshield

- Compute and intelligence through xAI

That opens up entirely new possibilities.

AI delivered over a global network that SpaceX controls. Enterprise services that bundle connectivity and compute. Secure government solutions combining communications and intelligence.

This is where the long-term upside sits. Not just connecting users, but owning the infrastructure that delivers both connectivity and intelligence.

4) The IPO is About Firepower

The valuation numbers around SpaceX’s IPO gets attention. Reports are already discussing a $1.5T plus valuation, according to the Financial Times.

But the more important angle is capital. SpaceX is an extremely capital-intensive business.

It is funding:

- Continuous satellite deployment

- Starship development

- Ground network expansion

- AI compute infrastructure

A large IPO gives it the ability to accelerate all of this at once. And that matters.

Because this is becoming a scale race. More satellites means better coverage. Better coverage means more customers. More customers funds more deployment.

Layer AI on top of that, and the flywheel becomes even stronger. Capital is not just a nice to have here. It is a strategic weapon.

What Does the SpaceX IPO Mean for Telecoms?

This is where it becomes real. Starlink is no longer just solving rural connectivity.

It is moving into:

- Aviation

- Maritime

- Enterprise backup

- Public safety

- Logistics

- Cross-border connectivity

And most importantly, direct to cell. This is the inflection point.

Starlink is already integrating with mobile operators globally. It behaves like a roaming partner, extending coverage beyond terrestrial networks.

But over time, it could reshape the economics of coverage itself.

For operators, that creates pressure. Roaming margins could compress. Coverage differentiation becomes harder.

The “always connected” experience may shift away from the operator brand.

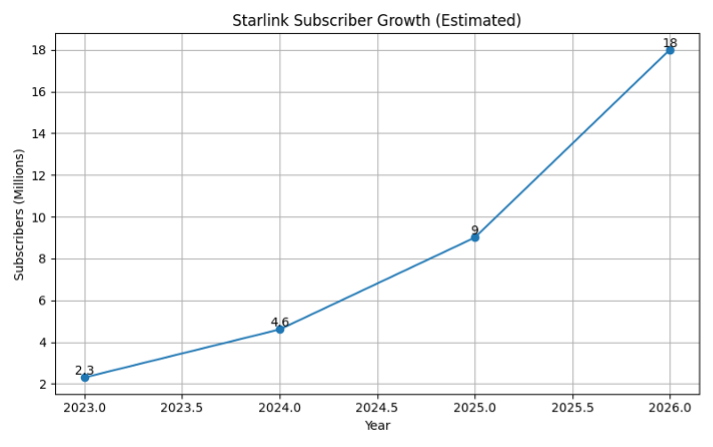

Figure 2 – Adoption is compounding faster than most telecom growth curves we’ve seen.

Figure 2 – Adoption is compounding faster than most telecom growth curves we’ve seen.

The MVNO Angle

For MVNOs and digital telco platforms, this is not just a threat. It is also a major opportunity.

MVNOs are structurally more flexible.

They can move faster to:

- Integrate satellite as a coverage layer

- Build global connectivity propositions

- Create new pricing models around availability and resilience

- Target specific use cases like travel, field work, and enterprise mobility

In many ways, this plays directly into the strengths of platform-led telecom models.

The question is not whether to compete with Starlink. It is how to compose with it.

The Bottom Line

SpaceX is not going public as a space company.

It is going public as a global infrastructure platform.

Starlink is the revenue engine. Launch is the moat. AI is the upside. Capital is the accelerator.

For telecoms, this is a structural shift.

A new player is emerging that controls its own network, its own deployment, and increasingly its own compute layer.

That combination is rare. And the industry has not fully adjusted to it yet.

Frequently Asked Questions

How big is Starlink today, and how fast is it growing?

Starlink is already the core revenue engine for SpaceX, with estimated 2024 revenue of $7.5–8B and 2025 revenue of $11–12B—50%+ growth at multi-billion scale. Some forecasts see ~$15B by 2026, effectively doubling in two years. At that point, it shifts from being seen as a satellite product to a global connectivity platform and a piece of core telecom infrastructure.

Why is SpaceX’s real moat launch, not satellites?

SpaceX controls launch frequency, cost, and capacity—and crucially uses that capacity for itself. That lets it deploy and refresh the Starlink network faster and cheaper than rivals, creating a compounding advantage no telco (and few satellite players) can match. Amazon’s Kuiper is credible but earlier in its cycle and lacks SpaceX’s integrated launch cadence, which is the foundation of Starlink’s differentiated scaling.

How does the xAI acquisition change SpaceX’s trajectory?

It broadens SpaceX from connectivity and launch into a vertically integrated platform that combines Starlink (connectivity), Starshield (government/defense services), and xAI (compute and intelligence). This enables new offerings such as AI delivered over a global network, enterprise bundles that marry connectivity and compute, and secure government solutions that fuse communications with intelligence. The long-term upside is owning the infrastructure for both connectivity and intelligence end-to-end.

What’s the real point of the IPO beyond the headline valuation?

Firepower. SpaceX operates in a capital-intensive arena and needs funds to accelerate satellite deployment, Starship development, ground network buildout, and AI compute infrastructure. This is a scale race with a flywheel—more satellites drive better coverage, which attracts more customers, which funds more deployment. Capital isn’t optional; it’s a strategic weapon to reinforce that flywheel.

What does this mean for telecom operators and MVNOs?

Starlink is moving far beyond rural access into aviation, maritime, enterprise backup, public safety, logistics, cross-border connectivity, and—critically—direct to cell. As it integrates with mobile operators like a roaming partner, roaming margins may compress, coverage-based differentiation weakens, and the “always connected” experience can shift away from operator brands. MVNOs, however, can capitalise: they’re nimbler and can integrate satellite as a coverage layer, build global propositions, create pricing tied to availability/resilience, and target use cases like travel, field work, and enterprise mobility. The strategic move isn’t to compete with Starlink, but to cooperate with it.